Influencer marketing: A matter of liability and ethics

22 May 2025

The use of celebrities and influencers in social media marketing is increasing. However, this has come with cases of false advertising where consumers bear negative consequences.

RMIT Vietnam launches Centre for Business and Emerging Technologies

16 May 2025

On 16 May, RMIT Vietnam launched the Centre for Business and Emerging Technologies (CBET) advancing its commitment to Vietnam and ASEAN’s (Association of Southeast Asian Nations) digital transformation.

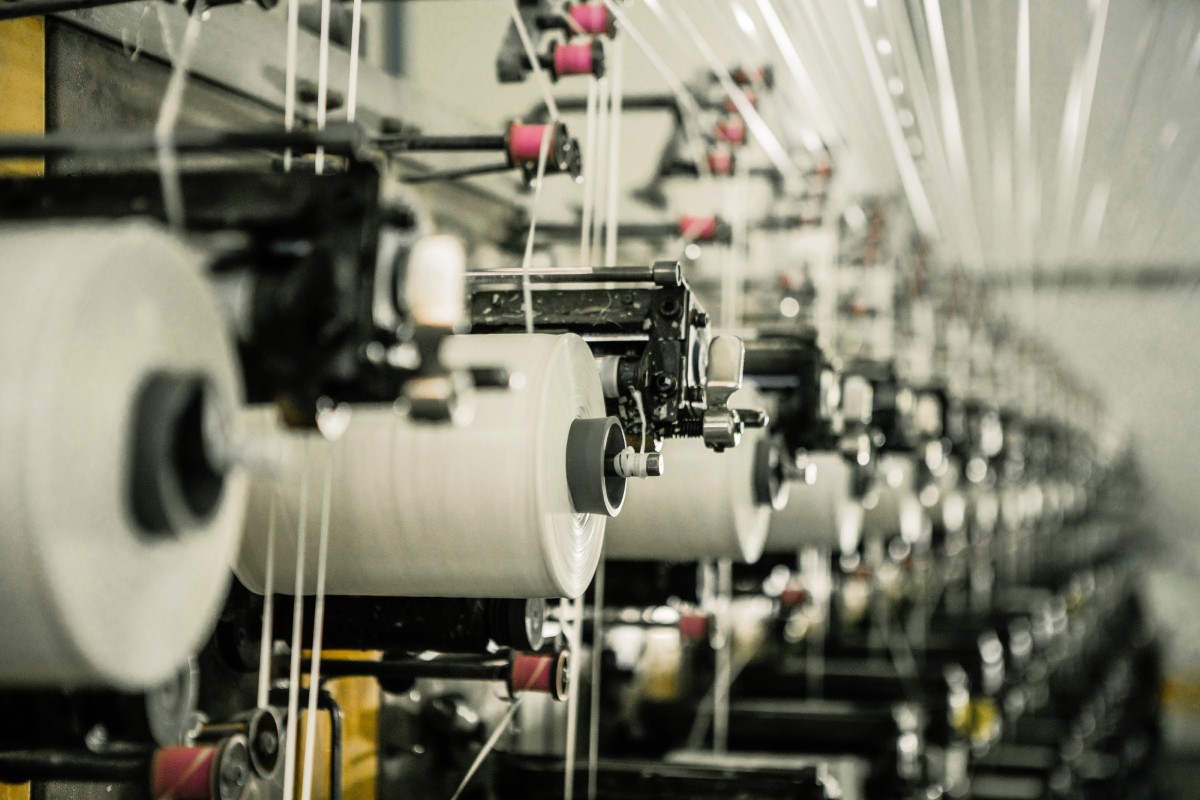

Impact of US tariffs on Vietnam’s textile, clothing and footwear sector

15 May 2025

The adjustments in the US tariffs are poised to reshape Vietnam’s textile, clothing and footwear industry, prompting businesses to reassess their strategies and operations.

Vietnam tourism’s soft power: Cinema and music should be the new focus

14 May 2025

Leveraging its growing tourism appeal, Vietnam can further boost its global influence through cinema and music.